What Is Maintenance and Cure in Maritime Law?

In maritime work, an injury can leave you stranded without pay or medical help. The law steps in with a safety net called maintenance and cure. This article breaks down what that term means, who can claim it, what it pays for, how long it lasts, how to start a claim, and the most common roadblocks you might hit.

By the end you’ll know the exact steps to protect your rights and where to turn for help.

What Is Maintenance and Cure?

Maintenance and cure is a two‑part benefit rooted in centuries‑old admiralty law. "Maintenance" covers everyday living costs while you recover, such as food, rent, and utilities. "Cure" pays for all reasonable medical treatment related to the injury until you reach maximum medical improvement (MMI). The doctrine is “no‑fault,” meaning you do not have to prove the shipowner was negligent to receive it.

Because the rule is so old, courts look to historic cases and statutes to decide what counts as reasonable. For example, the Supreme Court has held that any doubt in a seaman’s claim should be resolved in his favor. This low burden of proof makes the benefit powerful, but only if you can show the injury happened while you were serving the vessel.

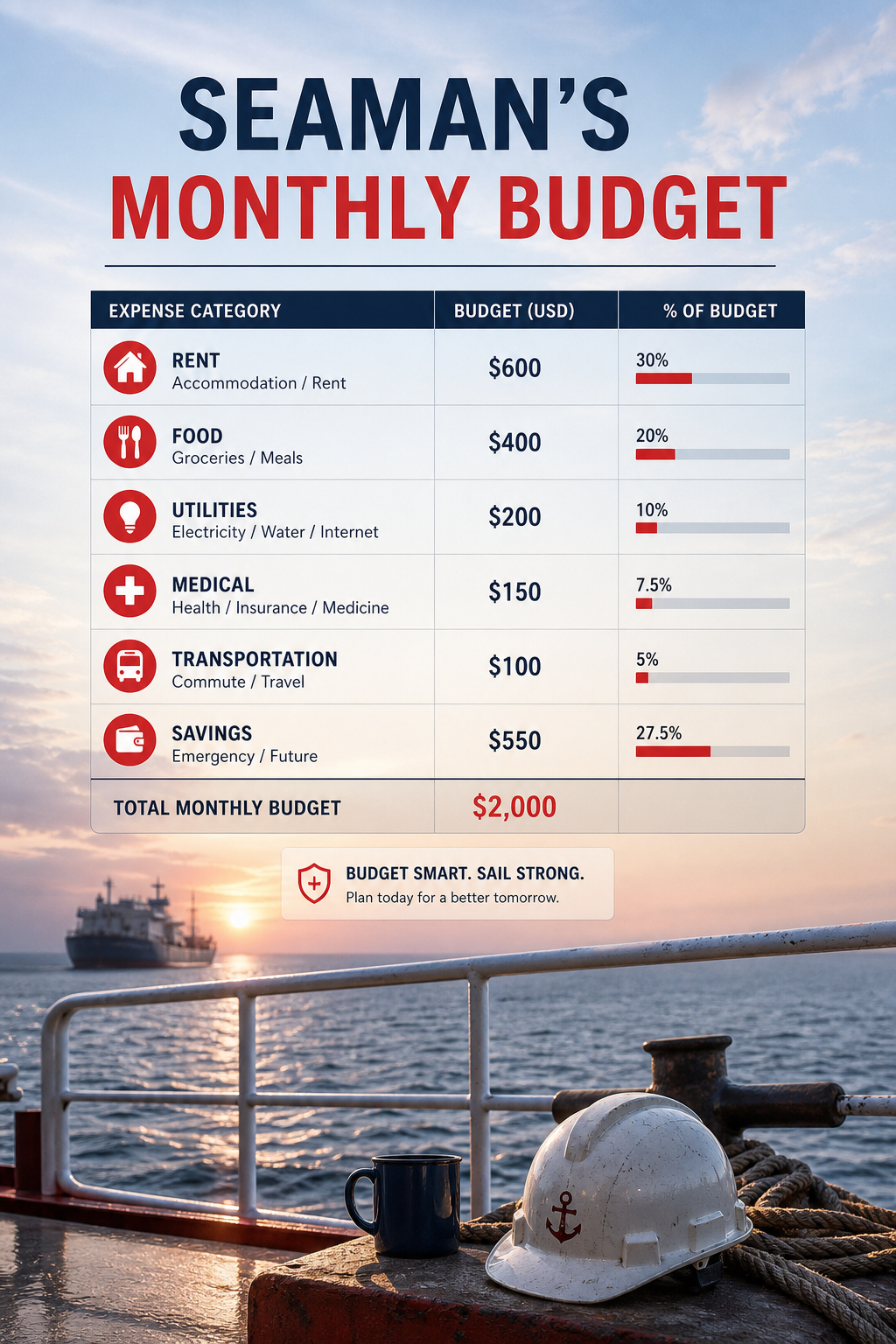

In practice, maintenance payments are often set at a flat daily rate. Many employers use a historic figure of $15‑$30 per day, even though modern cost‑of‑living data show that a fair rate is closer to $80‑$100 per day in places like Texas. When the amount is too low, a lawyer can audit your actual expenses, rent receipts, utility bills, grocery tabs, and demand a proper rate.

Medical "cure" covers everything from X‑rays and surgeries to physical therapy and prescription drugs. The shipowner must pay even if you see a doctor of your choice, though you may have to attend at least one exam with the company doctor.

Understanding the split helps you track what you can claim and where disputes usually arise. Employers often try to trim the maintenance amount or declare you at MMI early to stop medical payments.

For a concise definition, see Wikipedia’s entry on maintenance and cure. It outlines the historical roots and modern application in clear language.

Who Is Entitled to Maintenance and Cure?

Eligibility hinges on the legal definition of a "seaman." Courts look at three factors: the vessel must be capable of moving under its own power, it must be engaged in interstate or foreign commerce, and the worker must spend at least 30 % of his or her time on the vessel. Jobs that meet the test range from deckhands and engineers to cooks, fishermen, and even longshoremen.

If you fit those criteria and you are injured or become ill while performing duties, or even if a pre‑existing condition flares up during service, you qualify for maintenance and cure. The injury does not need to be caused by the employer; it only needs to occur while you are answerable to the ship’s call to duty.

Because the rule is no‑fault, you do not have to show negligence. However, you must prove the injury happened in the scope of employment. That often means gathering witness statements, accident reports, and detailed medical records that tie the condition to your time on board.

Imagine you slip on a wet deck and break your wrist. You would file a claim showing the incident report, photos of the deck, and a doctor’s note linking the fracture to the fall. Even if you later discover the wrist was weakened by a prior sprain, the claim can still succeed as long as the work‑related event aggravated it.

Some workers think they are excluded because they were off‑duty or on shore leave. The law says that if the injury occurs while you are still considered “in service”, for example, traveling to the vessel or performing duties in a port, you remain covered.

Employers sometimes challenge seaman status, especially for workers who split time between land‑based and vessel‑based duties. In those cases, a lawyer will compare your work logs to the 30 % rule and cite precedents that favor the crew member.

When you’re unsure whether your role meets the seaman test, a quick review of the Cornell Law School’s legal encyclopedia can clarify the statutory elements.

What Does Maintenance and Cure Cover?

Maintenance payments cover basic living expenses. That includes rent or hotel costs, utilities, food, and modest personal items like clothing needed for daily life. The amount should reflect the actual cost of maintaining your standard of living on land, not the cheaper “on‑board” rates some owners try to impose.

To prove what’s reasonable, keep every receipt. A spreadsheet that totals your monthly rent, electricity, water, internet, and groceries provides solid evidence. If you’re hospitalized, the ship must still pay your home expenses because you cannot earn wages while you recover.

Cure benefits are broader. They include:

- Hospital stays and surgeries

- Doctor visits and specialist consultations

- Diagnostic tests such as X‑rays, MRIs, and CT scans

- Prescribed medication and medical devices

- Physical therapy, occupational therapy, and rehabilitation

- Transportation to and from medical appointments

- Home health aide services when you cannot care for yourself

Note that once you reach MMI, cure stops. MMI means a qualified physician says further treatment won’t improve your condition. It does not mean you are fully healed; lingering pain can remain, but the law caps the medical obligation.

Some costs are excluded. Elective procedures, cosmetic surgery, and treatments for unrelated conditions are not covered. Also, any care you receive after MMI, unless a new injury occurs, won’t be reimbursed under maintenance and cure.

Below is a quick reference table that shows typical covered items versus common exclusions.

Because the shipowner can set a low maintenance rate, many seamen hire a lawyer to audit their real expenses and push for a fair daily amount.

Duration and Termination of Maintenance and Cure

Both maintenance and cure continue as long as you need them. Maintenance stops when you are no longer unable to work or when you have returned to a normal living situation. Cure ends when a doctor declares you have reached maximum medical improvement (MMI). The moment MMI is reached, the shipowner can legally stop paying for further medical care.

However, the law also recognizes permanent disability. If you are left with a lasting impairment, you may still receive maintenance payments even after MMI, because you still cannot support yourself fully.

Employers sometimes try to declare MMI early. They may present an independent medical examiner (IME) who says you are “cured” even if you still have pain. If that happens, you can challenge the IME’s findings by getting a second opinion from a specialist you trust. The burden of proof shifts to the employer to show the MMI determination is reasonable.

Another way benefits end is if you return to work in a capacity that provides sufficient income. The law does not force you to stay on disability; you can accept light‑duty work while still receiving maintenance, as long as you still need medical treatment or cannot fully support yourself.

If the shipowner refuses to continue payments after you have shown ongoing need, you may sue for breach of the maintenance and cure duty. Courts will look at the totality of your expenses, medical reports, and any evidence of the employer’s bad faith.

Punitive damages are rare but possible when an employer acts with willful disregard, such as knowingly paying a low rate while you can prove higher costs. In such cases, a judge may award extra money to punish the bad conduct.

For a clear legal definition of the duty, see Cornell Law School’s explanation of maintenance and cure. It outlines the obligations and the standards courts use to decide when benefits end.

How to File a Maintenance and Cure Claim

Filing starts the moment you are injured. First, report the incident to your supervisor in writing within seven days. The report should include the date, time, location, what you were doing, and any witnesses.

Next, gather evidence. Collect all medical records, bills, and receipts for living expenses. Get contact info for anyone who saw the accident. The more documentation you have, the stronger your claim.

Then, submit a formal demand to the shipowner or the insurer. Your demand letter should list the maintenance amount you are seeking, attach your expense spreadsheet, and cite the medical reports that show you have not yet reached MMI.

If the employer balks, you may need to file a lawsuit in federal admiralty court. That filing includes a complaint that outlines the injury, your seaman status, and the benefits you are owed. The court will issue a summons to the shipowner, who must then respond.Throughout the process, avoid signing any statements or recordings that could be used against you. Insurance adjusters often try to get a “sworn statement” that downplays your injuries. If they ask, politely decline and ask for a lawyer.

Many seamen think they can handle the paperwork alone, but a seasoned maritime attorney can help you handle the legal jargon, calculate a fair maintenance rate, and push back against premature MMI claims.

Our team at Offshore Injury Lawyer Guide: Protect Your Rights on the High Seas regularly assists crew members with these steps, ensuring the claim is filed correctly and on time.

Common Disputes and Legal Defenses

Disputes usually fall into three buckets: the amount of maintenance, the timing of cure, and the seaman status itself. Employers may argue that you are not a seaman because you spend less than 30 % of your time on a vessel. They may also claim the injury was caused by your own negligence, which can limit the benefits.

Another frequent tactic is to assert that you have already reached MMI. They will present an IME who says further treatment is unnecessary. To fight that, you can obtain a second opinion from a specialist who can demonstrate ongoing limitations.

When the shipowner disputes the maintenance rate, they often cite a historic flat rate of $15‑$30 per day. You can counter by presenting a cost‑of‑living analysis that shows your actual rent, utilities, and food costs are far higher. Courts generally favor the higher, documented amount.

In some cases, the employer may hide a pre‑existing condition and claim the injury is unrelated to work. The law says that if a pre‑existing condition worsens while you are in service, you still qualify for maintenance and cure, unless you caused the aggravation through willful misconduct.

Employers sometimes try to recover payments they think were made in error. Recent case law makes clear that if a seaman concealed a prior injury, the employer may be able to recoup those amounts, but the burden is on the employer to prove the concealment.

Defenses that work for the employer include proving you were not answerable to the ship’s call to duty at the time of the incident, or that the injury occurred on land away from the vessel and unrelated to your maritime duties.

When a dispute escalates, a judge may order the shipowner to pay not only the owed maintenance and cure but also attorney’s fees and, in egregious cases, punitive damages. That extra pressure encourages owners to settle fairly early.

Frequently Asked Questions

What if I miss the 7‑day reporting deadline?

Missing the deadline does not automatically bar you from recovery, but it makes the employer’s job easier. You’ll need to explain why you couldn’t report sooner, perhaps you were unconscious or in a remote location. Provide any supporting evidence, such as a doctor’s note stating the delay was medically necessary. Courts may still grant benefits if the delay was reasonable.

Can I receive maintenance and cure while I’m on a short‑term shore job?

Yes, if you remain answerable to the ship’s call of duty and the injury or illness originated while you were on board. Working a temporary shore job does not automatically end your claim, as long as you still need medical treatment or cannot fully support yourself.

Do I have to use the shipowner’s doctor?

No. You may choose any qualified physician for treatment. The shipowner can require you to see their doctor once for an initial exam, but you retain the right to continue care with your own doctors after that.

How is the daily maintenance rate calculated?

The rate should reflect the actual cost of maintaining a normal standard of living on land. Collect rent receipts, utility bills, grocery receipts, and any other regular expenses. A lawyer can compare those costs to the shipowner’s offered rate and argue for a higher amount based on documented evidence.

What is “maximum medical improvement” (MMI) exactly?

MMI is the point at which a qualified physician determines that further medical treatment will not substantially improve your condition. It does not mean you are fully healed; lingering pain or limitations can remain. Cure benefits stop at MMI, but maintenance may continue if you still cannot work.

Can I sue for additional damages beyond maintenance and cure?

Yes. If the injury was caused by negligence or an unseaworthy vessel, you can file a separate Jones Act claim for pain and suffering, lost wages, and other damages. Maintenance and cure is a no‑fault benefit, but it does not preclude other compensation.

What if the shipowner refuses to pay any amount?

If the shipowner outright refuses, you can file a breach of maintenance and cure lawsuit in federal admiralty court. The court can order payment of the owed benefits, attorney’s fees, and, in extreme cases, punitive damages for bad‑faith conduct.

Do I need a lawyer to get maintenance and cure?

You are not required to have an attorney, but handling the legal nuances, especially when the employer disputes the claim, can be complex. A lawyer familiar with maritime law can help you gather proper evidence, calculate a fair maintenance rate, and protect your rights against premature MMI claims.

Conclusion

Maintenance and cure is a vital safety net for anyone who works at sea. It guarantees you won’t be left without food, shelter, or medical care simply because you were injured while serving a vessel. Knowing who qualifies, what the benefits cover, how long they last, and the exact steps to file a claim puts you in a strong position to protect your rights.

If you’re dealing with a denied claim or an under‑payment, the next smart move is to talk to a maritime attorney who can audit your expenses, challenge premature MMI declarations, and, if needed, take the case to court. For a deeper look at related maritime rights, for more details on additional compensation you might be owed.

Remember: act quickly, keep every piece of paperwork, and don’t let an employer’s lowball offer dictate your recovery. The law is on your side, use it.